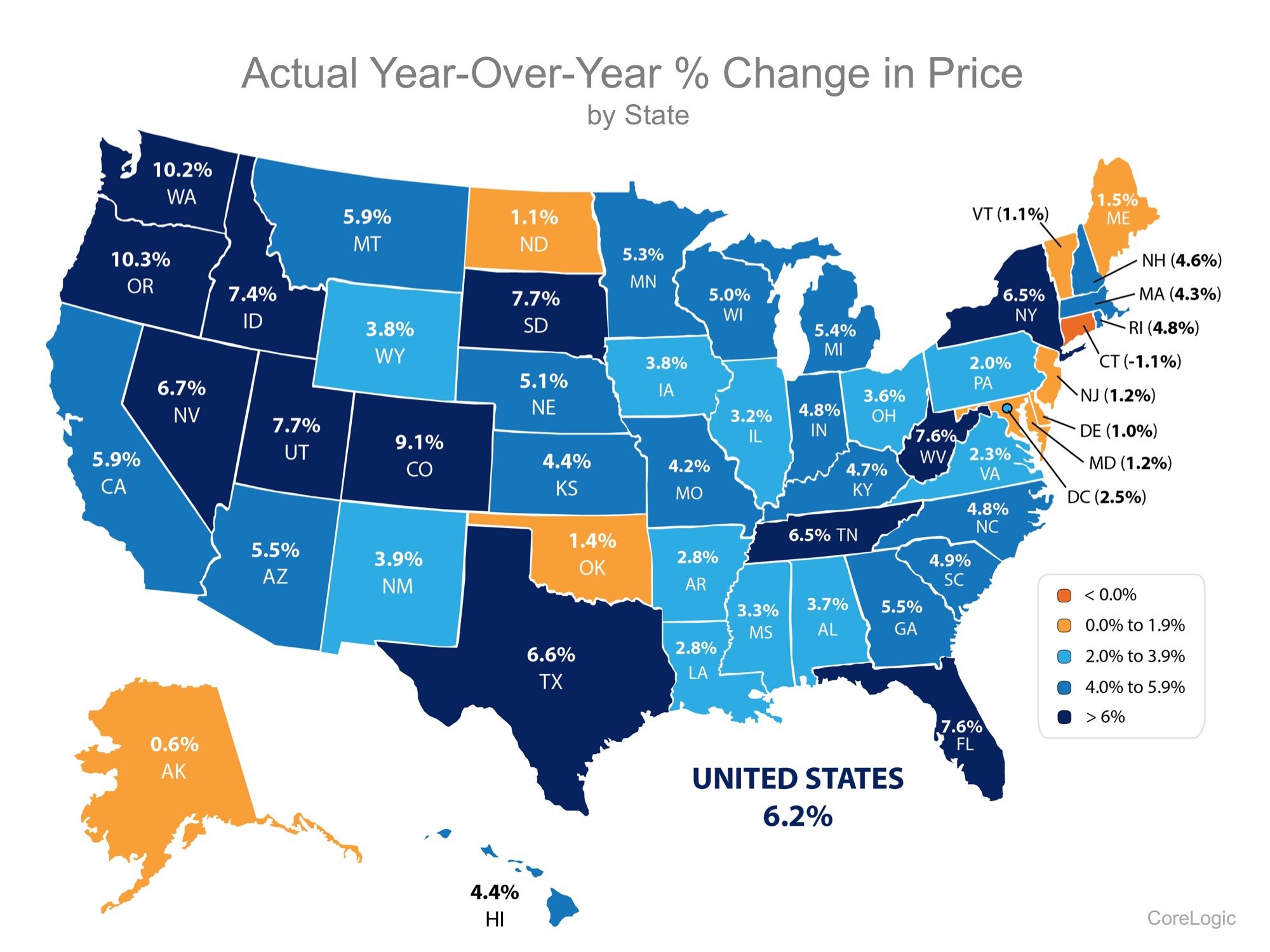

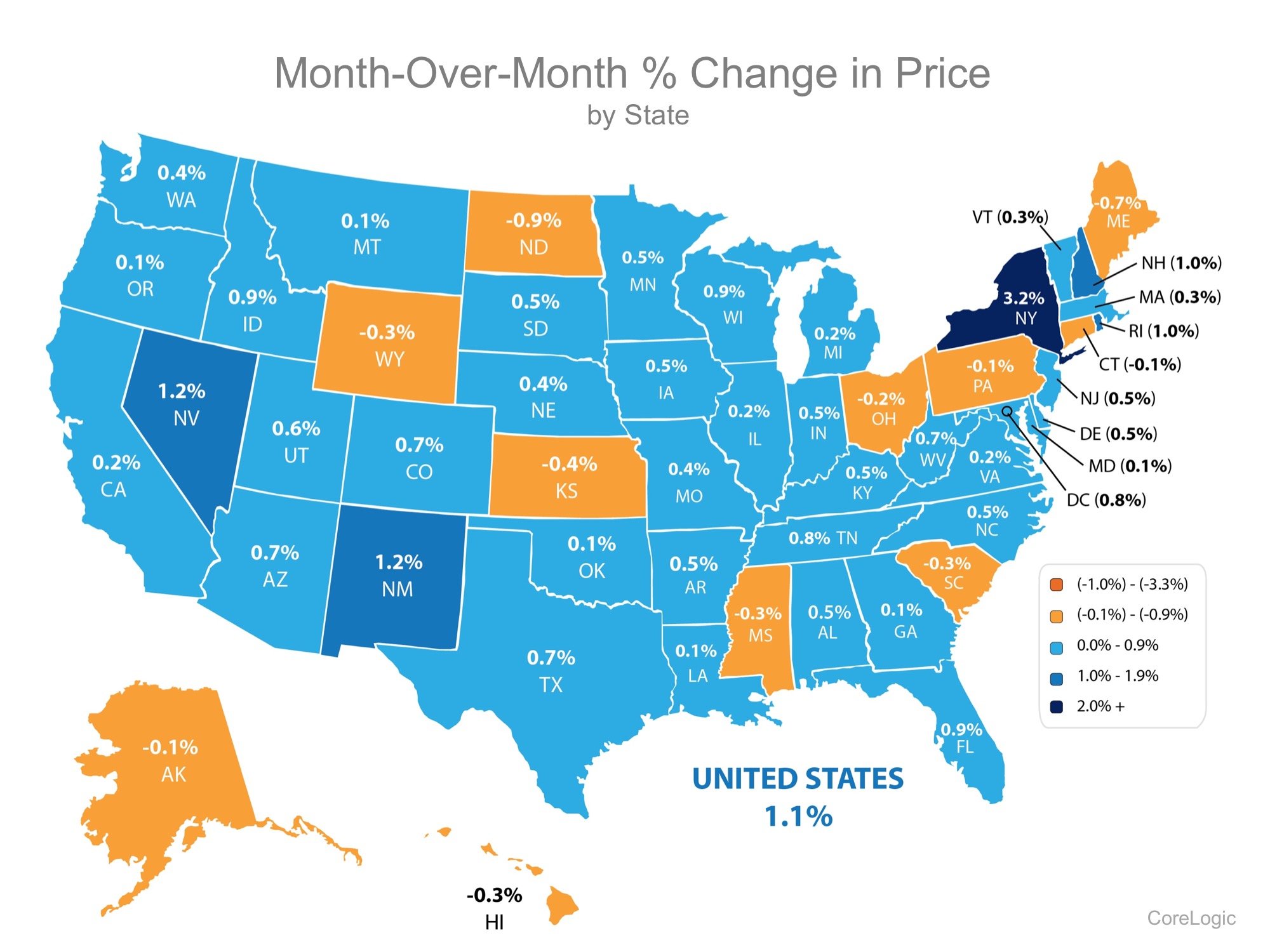

CoreLogic released their most current Home Price Index last week. In the report, they revealed home appreciation in three categories: percentage appreciation over the last year, over the last month and projected over the next twelve months.

Here are state maps for each category:

The Past – home appreciation over the last 12 months

The Present – home appreciation over the last month

The Future – home appreciation projected over the next 12 months

Bottom Line

Homes across the country are appreciating at different rates. If you plan on relocating to another state and are waiting for your home to appreciate more, you need to know that the home you will buy in another state may be appreciating even faster.

If you are debating purchasing a home right now, you are probably getting a lot of advice. Though your friends and family will have your best interest at heart, they may not be fully aware of your needs and what is currently happening in the real estate market.

Ask yourself the following 3 questions to help determine if now is actually a good time for you to buy in today’s market.

1. Why am I buying a home in the first place?

This truly is the most important question to answer. Forget the finances for a minute. Why did you even begin to consider purchasing a home? For most, the reason has nothing to do with money.

For example, a recent survey by Braun showed that over 75% of parents say “their child’s education is an important part of the

I asked you all to send me your questions about buying and selling real estate, and I got two good questions from Bob that I’d like to answer for you today.

Bob asks, “For those of us who may not be planning to list our homes now, what improvements should we make to the interior and exterior of our homes in priority order?”

The very first priority should be to look at each room, starting at the front of the house. Look at your front porch and the foyer of your home. Do you have a lot of items cluttering the area? You should have no more than one, two, or three items on a surface.

Walk by every room and look at each of your three items, and think

Stunning 6 bedroom, 5 ½ bath brick Colonial on quiet cul-de-sac with 2 story foyer, curved stairway, gourmet kitchen & breakfast room with wall of windows overlooking yard, patio & deck. Living room with fireplace, formal dining room, huge family room & office with buit-ins. Lower level rec room, exercise room & kitchenette. Great location just over the DC line.

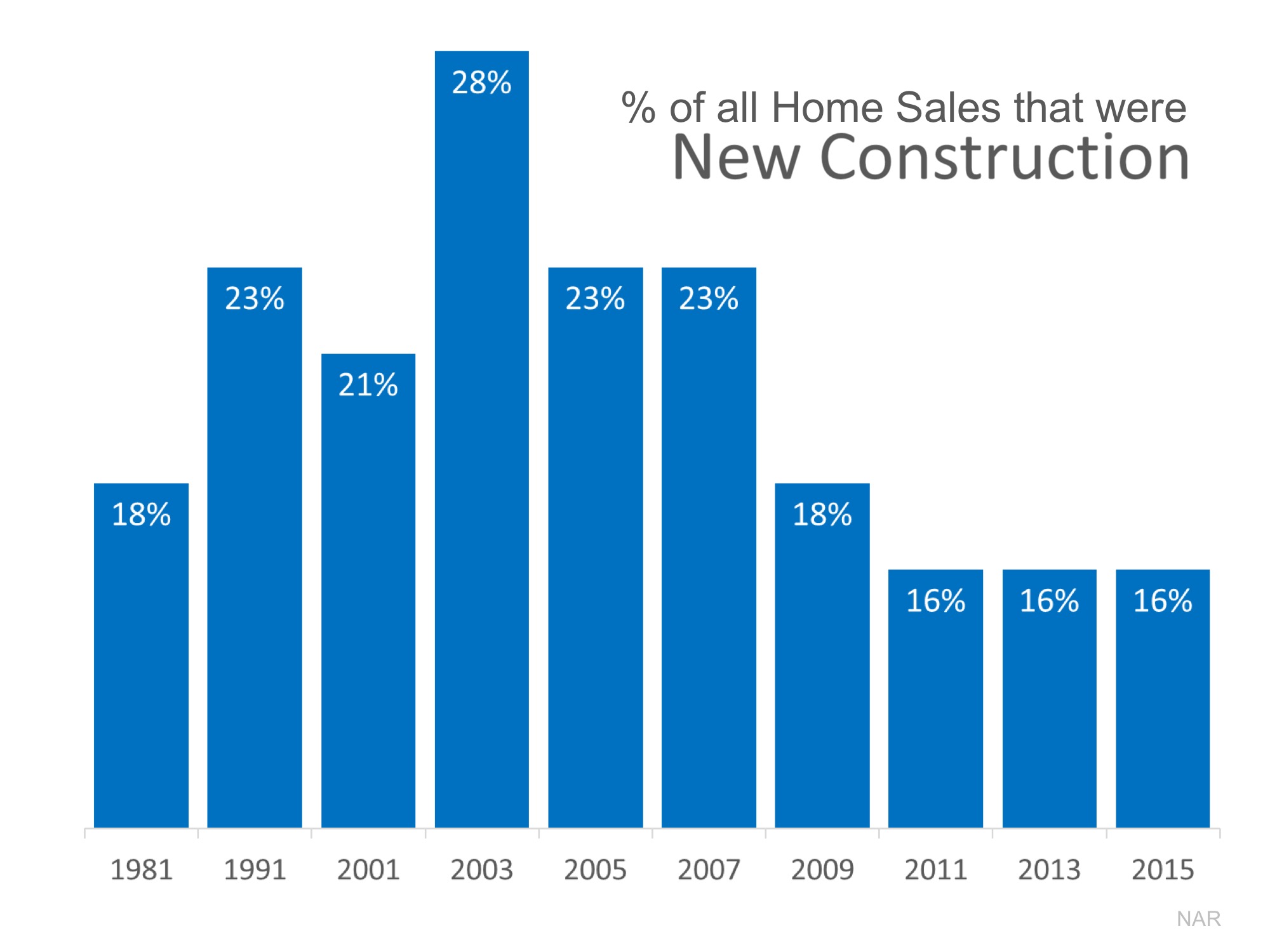

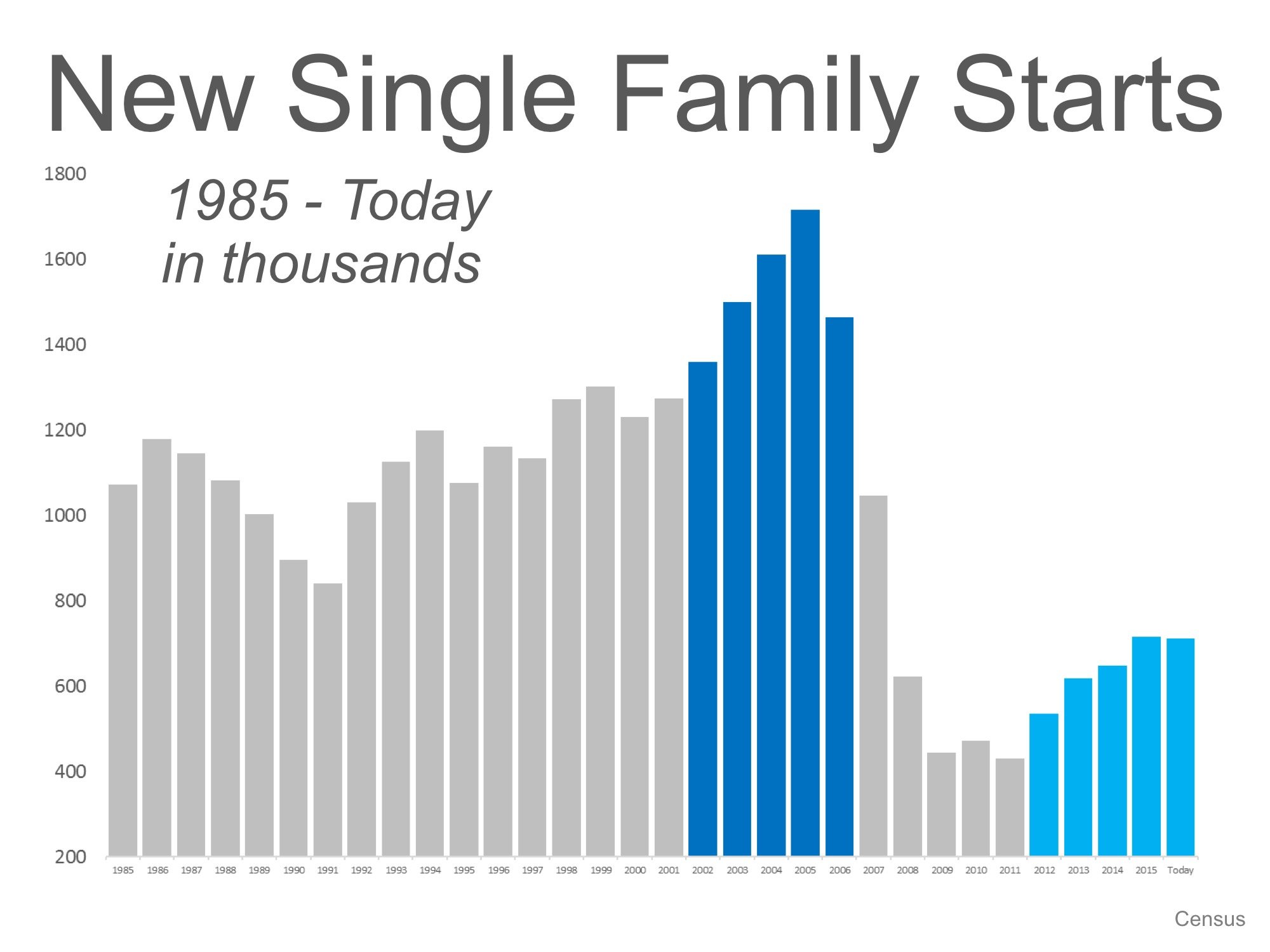

The number of new home sales is far off historic norms. The National Association of Realtors (NAR) just reported that the percentage of all house sales that were newly constructed homes has fallen to the lowest numbers in forty years. Here is a graph showing the percentages:

This should come as no surprise as the number of new housing starts has fallen dramatically over the last several years:

Bottom Line

We need more new construction for two reasons:

It will relieve some of the pent-up buying demand that is causing price appreciation to continue to increase well above historic norms.

It will give better opportunities to many current homeowners who want to sell but can’t find an adequate home to move in to.

There are many potential homebuyers, and even sellers, who believe that you need at least a 20% down payment in order to buy a home, or move on to their next home. Time after time, we have dispelled this myth by showing that there are many loan programs that allow you to put down as little as 3% (or 0% with a VA loan).

If you have saved up your down payment and are ready to start your home search, one other piece of the puzzle is to make sure that you have saved enough for your closing costs.

Freddie Mac defines closing costs as:

“Closing costs, also called settlement fees, will need to be paid when you obtain a mortgage. These are fees charged by people representing your purchase, including your lender, real estate agent, and other third

In today’s market, with home prices rising and a lack of inventory, some homeowners may consider trying to sell their home on their own, known in the industry as a For Sale by Owner (FSBO). There are several reasons why this might not be a good idea for the vast majority of sellers.

Here are the top five reasons:

1. Exposure to Prospective Buyers

Recent studies have shown that 88% of buyers search online for a home. That is in comparison to only 21% looking at print newspaper ads. Most real estate agents have an internet strategy to promote the sale of your home. Do you?

2. Results Come from the Internet

Where did buyers find the home they actually purchased?

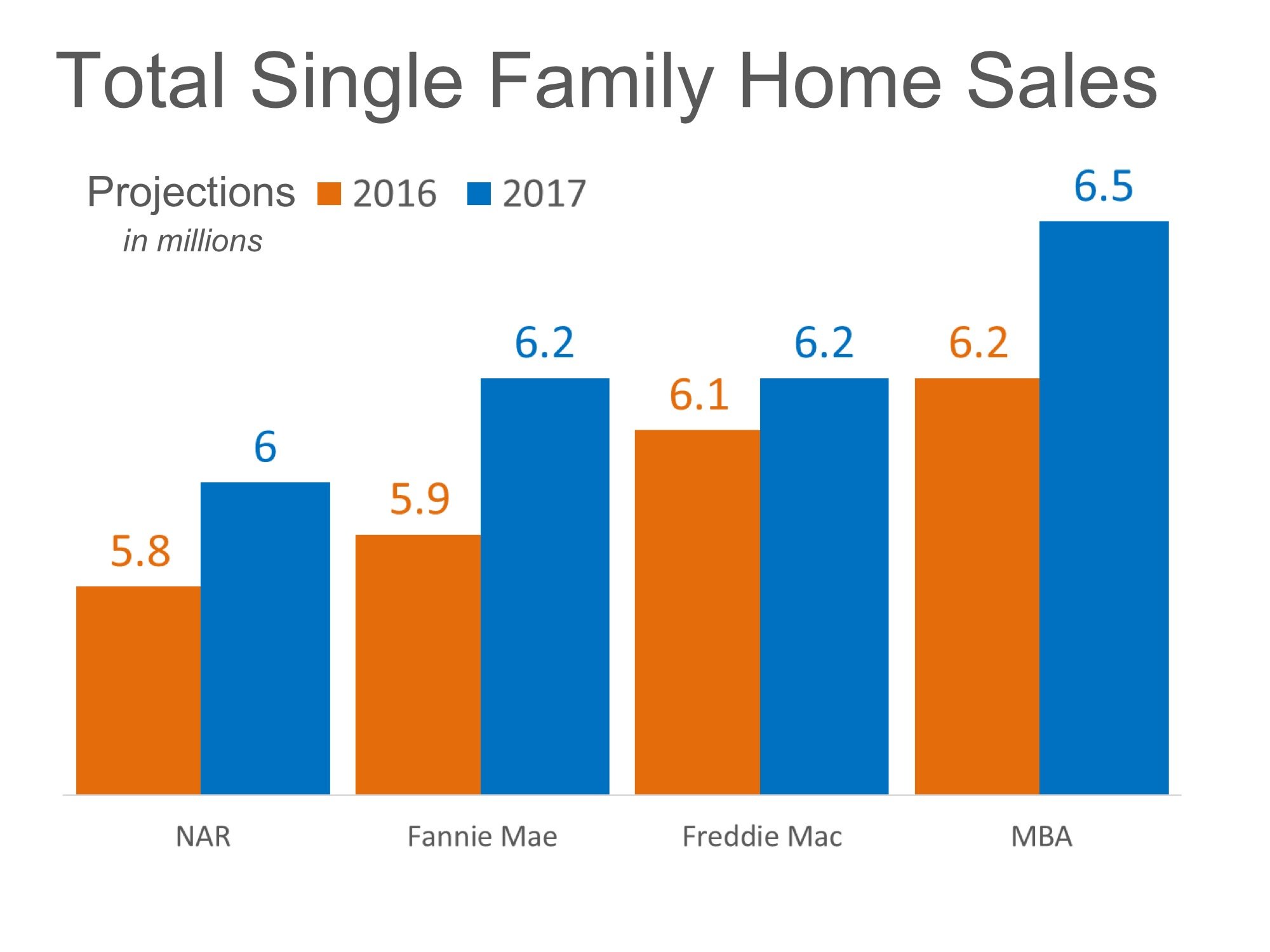

The National Association of Realtors, The Mortgage Bankers’ Association, Freddie Mac and Fannie Maeare all projecting that home sales will increase in 2017. Here is a chart showing what each entity is projecting in sales for this year and the next.

As we can see, each is projecting sizable increases in home sales next year. If you have considered selling your house recently, now may be the time to put it on the market.

Thinking about buying or selling? You probably have questions. CLICK the link below for a free, confidential 17 minute conversation... LET'S TALK!

![Mortgage Rates by Decade Compared to Today [INFOGRAPHIC] | Simplifying The Market](http://www.simplifyingthemarket.com/wp-content/uploads/2016/10/20161007-Mortgage-Rates-STM.jpg)

.jpg)

![Lack of Existing Home Sales Inventory Impacting Sales [INFOGRAPHIC] | Simplifying The Market](http://www.simplifyingthemarket.com/wp-content/uploads/2016/09/20160930-STM-ENG.jpg)