Recently released data from the National Center for Health Statistics revealed that 1.3 million Millennial women gave birth for the first time in 2015. There are now over 16 million women in this generation who have become mothers.

“All told, Millennial women (those born between 1981 to 1997) accounted for about eight in ten (82%) of U.S. births in 2015.”

The data also shows that this generation has waited until later in life to become parents as only 42% of Millennial women were moms in 2014, compared to 49% of Generation X at the same age. APew Research Center article discussing the data, points to social influences that may have contributed to the delay:

“The rising age at first birth is hardly limited to the Millennial

In many markets across the country, the number of buyers searching for their dream homes greatly outnumbers the amount of homes for sale. This has led to a competitive marketplace where buyers often need to stand out. One way to show you are serious about buying your dream home is to get pre-qualified or pre-approved for a mortgage before starting your search.

Even if you are in a market that is not as competitive, knowing your budget will give you the confidence of knowing if your dream home is within your reach.

Freddie Mac lays out the advantages of pre-approval in the My Home section of their website:

“It’s highly recommended that you work with your lender to get pre-approved before you begin house hunting. Pre-approval will tell you how

Welcome back to another edition of “What’s Working Now!" Today we’re going to discuss... wait, shh, listen to the lament of today's serious buyers, "There are no homes for sale right now!"

It’s true—there is a continuing trend in our market that has created an incredible opportunity for home sellers to make more money. The weather is cold outside and many are under the impression that no one is out looking at homes right now.

In reality, buyers are saying they want to buy, they are well-qualified to buy, and there are no homes for sale right now. If I were to put your home on the market now, it would probably be sold within a week or sooner! Just the other day, I had an open house Sunday afternoon and Sunday night the

According to data from the U.S Census bureau, there are approximately 76.4 million baby boomers living in the United States today. Contrary to what many think, there are very different segments within this generation, and one piece that sets them apart are their housing needs.

John McManus, editorial director of Hanley Wood’s Residential Group says his company “is focusing on the preferences of the younger half, or second-wave baby boomers, as they exhibit different needs than the older boomers.”

What are ‘second-wave baby boomers’ looking for?

McManus says, “They are seeking a fun, dynamic lifestyle with a home that can also adjust to their changing needs in the future. Living space should either include accessibility features, such as

Many people wonder whether they should hire a real estate professional to assist them in buying their dream home or if they should first try to do it on their own. In today’s market: you need an experienced professional!

You Need an Expert Guide if You Are Traveling a Dangerous Path

The field of real estate is loaded with land mines; you need a true expert to guide you through the dangerous pitfalls that currently exist. Finding a home that is priced appropriately and is ready for you to move into can be tricky. An agent listens to your wants and needs, and can sift through the homes that do not fit within the parameters of your “dream home.”

A great agent will also have relationships with mortgage professionals and other experts that you

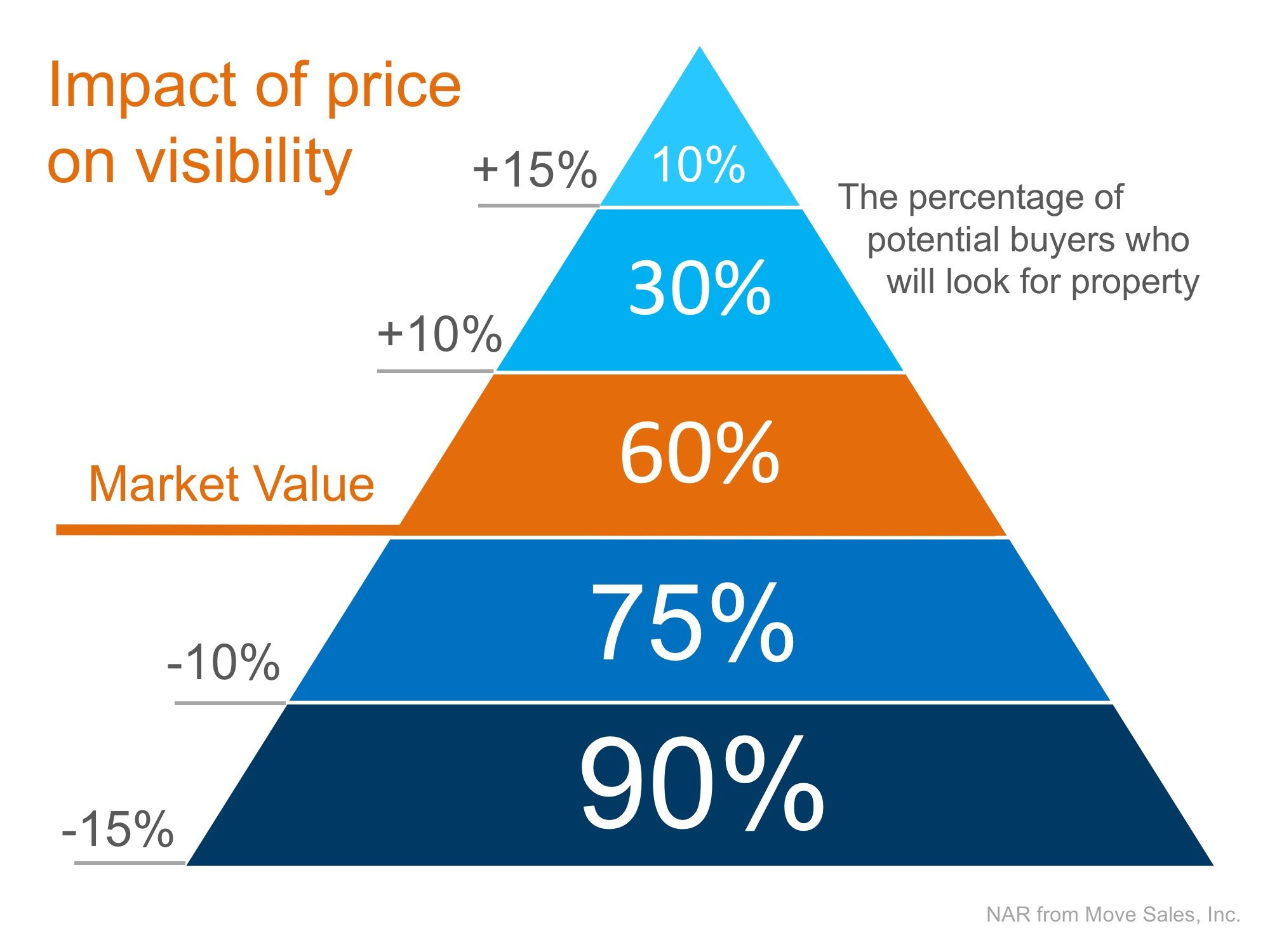

The residential housing market has been hot. Home sales have bounced back solidly and are now at their second highest pace since February 2007. Demand has remained strong throughout the winter as many real estate professionals are reporting bidding wars with many homes selling above listing price. What about your house?

If your house hasn’t sold, it is probably because of the price.

If your home is on the market and you are not receiving any offers, look at your price. Pricing your home just 10% above market value dramatically cuts the number of prospective buyers that will even see your house. See chart below.

Bottom Line

The housing market is hot. If you are not seeing the results you want, sit down with your agent and revisit

Stunning two level, 2 bedroom plus den, 2 1/2 bath condo in McLean Gardens with two entrances, wood floors, new washer/dryer & central air. New storm windows, screens & locks installed this summer. 1 dog, 2 cats, or 1 dog plus 1 cat permitted. Amazing location- pool, tot lot, public dog park, tennis court, playground, community garden, parkland trails, restaurants, shops, Giant & CVS.

Monthly Condo fee: $653.36 includes water, sewer, gas, trash removal, snow removal, maintenance of common areas, condominium liability insurance, reserve fund, professional management, tot lot, outdoor swimming pool, bike racks & BBQ areas.

The National Association of Realtors’ most recent Existing Home Sales Report revealed that, compared to last year, home sales are up dramatically in five of the six price ranges they measure.

Homes priced between $100-250K showed a 20.7% increase year-over-year. This is an impressive increase, showing that November was an excellent month for home sales in this price range.

But surprisingly, the 20.7% increase in sales in this range was not the highest percent change achieved, as sales of homes over $250,000 increased by double-digit percentages with sales in the $750,000- $1 million range showing the largest increase, up 43.2%!

As prices in many markets continue to accelerate, it is no surprise to see the percentage of homes in the higher

The latest Existing Home Sales Report from the National Association of Realtors (NAR) revealed a direct correlation between a lack of inventory and rising prices.

We are all familiar with the concept of supply and demand. As the demand for an item increases the supply of that same item goes down, driving prices up.

Year-over-year inventory levels have dropped each of the last 18 months, as inventory now stands at a 4.0-month supply, well below the 6.0-month supply needed for a ‘normal’ market.

The median price of homes sold in November (the latest data available) was $234,900, up 6.8% from last year and marking the 57th consecutive month with year-over-year gains.

NAR’s Chief Economist, Lawrence Yun had this to say:

![3 Tips for Making Your Dream of Buying a Home Come True [INFOGRAPHIC] | Keeping Current Matters](http://www.keepingcurrentmatters.com/wp-content/uploads/2017/01/3-Tips-KCM.jpg)