We often discuss the difference in family wealth between homeowner households and renter households. Much of that difference is the result of the equity buildup that homeowners experience over the time that they own their home. In a report recently released by the nonpartisan Employee Benefit Research Institute (EBRI), they reveal how valuable equity can be in retirement planning.

Craig Copeland, Senior Research Associate at EBRI, recently authored a report, Importance of Individual Account Retirement Plans and Home Equity in Family Total Wealth, in which he reveals:

“Individual account retirement plan assets, plus home equity, represent almost all of what families have to use for retirement expenses outside of Social Security and traditional

Many real estate economists have called on new home builders to ramp up production to help relieve the shortage of inventory of homes for sale throughout the United States. The added inventory would no doubt aid buyers in their search to secure their dream home, while also helping to ease price increases throughout the country.

Unfortunately for builders, there are many forces that are making it difficult for them to do just that!

Last week at the National Association of Real Estate Editors 51st Annual Conference, CoreLogic’s Chief Economist Frank Nothaft broke down the 4 ‘L’s of New Home Construction: Lots, Labor, Lumber, and Lending.

The concept of supply and demand is ripe in the new home construction industry. The four ‘L’s of new home

CoreLogic’s latest Equity Report revealed that 91,000 properties regained equity in the first quarter of 2017. This is great news for the country, as 48.2 million of all mortgaged properties are now in a positive equity situation.

Price Appreciation = Good News for Homeowners

Frank Nothaft, CoreLogic’s Chief Economist, explains:

“One million borrowers achieved positive equity over the last year, which means risk continues to steadily decline as a result of increasing home prices.”

Frank Martell, President and CEO of CoreLogic, believes this is a great sign for the market in 2017 as well, as he had this to say:

“Homeowner equity increased by $766 billion over the last year, the largest increase since Q2 2014. The rising cushion

The results of the latest Rent vs. Buy Report from Trulia show that homeownership remains cheaper than renting with a traditional 30-year fixed rate mortgage in the 100 largest metro areas in the United States.

The updated numbers actually show that the range is an average of 3.5% less expensive in San Jose (CA), all the way up to 50.1% less expensive in Baton Rouge (LA), and 33.1% nationwide!

Other interesting findings in the report include:

Interest rates have remained low and, even though home prices have appreciated around the country, they haven’t greatly outpaced rental appreciation.

With rents & home values moving in tandem, shifts in the ‘rent vs. buy’ decision are largely driven by changes in mortgage interest rates.

According to a recent report by Trulia, “buying is cheaper than renting in 100 of the largest metro areas by an average of 33.1%.” The report may have some people thinking about buying a home instead of signing another lease extension, but does that make sense from a financial perspective?

Ralph McLaughlin, Trulia’s Chief Economist explains:

“Owning a home is one of the most common ways households build long-term wealth, as it acts like a forced savings account. Instead of paying your landlord, you can pay yourself in the long run through paying down a mortgage on a house.”

The article listed five reasons why owning a home makes financial sense:

Here are four great reasons to consider buying a home today, instead of waiting.

1. Prices Will Continue to Rise

CoreLogic’s latest Home Price Index reports that home prices have appreciated by 7.1% over the last 12 months. The same report predicts that prices will continue to increase at a rate of 4.9% over the next year.

The bottom in home prices has come and gone. Home values will continue to appreciate for years. Waiting no longer makes sense.

2. Mortgage Interest Rates Are Projected to Increase

Freddie Mac’s Primary Mortgage Market Survey shows that interest rates for a 30-year mortgage have remained around 4%. Most experts predict that they will begin to rise over the next 12 months. The Mortgage Bankers Association, Fannie Mae,

Even in a seller’s market, it can be risky to wait for a better offer to come along. How do you know when to sign on the dotted line?

Welcome to the latest episode of “What’s Working Now!”

Everyone knows that a bird in the hand is worth two in the bush. As a seller, there is a real danger and risk to making a ready, willing, and able buyer wait.

If you’re a seller and you get two offers on a property, you need to remember that speed makes money. The sooner you respond, the more excited the buyer will be. The longer you wait, the more anxious the buyer will become. They’ll decide to sleep on it, or they may get nervous enough to bolt.

When you sign on the dotted line, the buyer will get very excited. They will start planning

Spacious one bedroom at the sought after Elizabeth condo. Updated kitchen, wood floors & great closet space. Luxury high rise at Metro with reserved parking, 24-hour front desk, beauty salon/ barber shop, convenience store, exercise room, library, meeting room, newspaper service, party room, indoor pool, sauna spa.

$888.67 per month includes water, sewer, heat, electricity, trash removal, snow removal, professional managmenet, maintenance, lawn care, master insturance policy, reserve fund and all amenities.

Beautifully renovated corner one bedroom plus den. Contemporary kitchen open to dining room, unique floor plan, unlike any other. Wood floors, high ceilings, washer & dryer, custom closets, peaceful private tree views from the balcony, and extra storage included. Luxury full service building, with valet service and 24 hour front desk, gym, amazing outdoor heated pool, dry cleaners, party room & more.

Monthly condo fee $1,463 includes utilities, cable tv, custodial services, maintenance, lawn care, water, sewer, professional management, master insurance policy, security, reserve fund and all amenities.

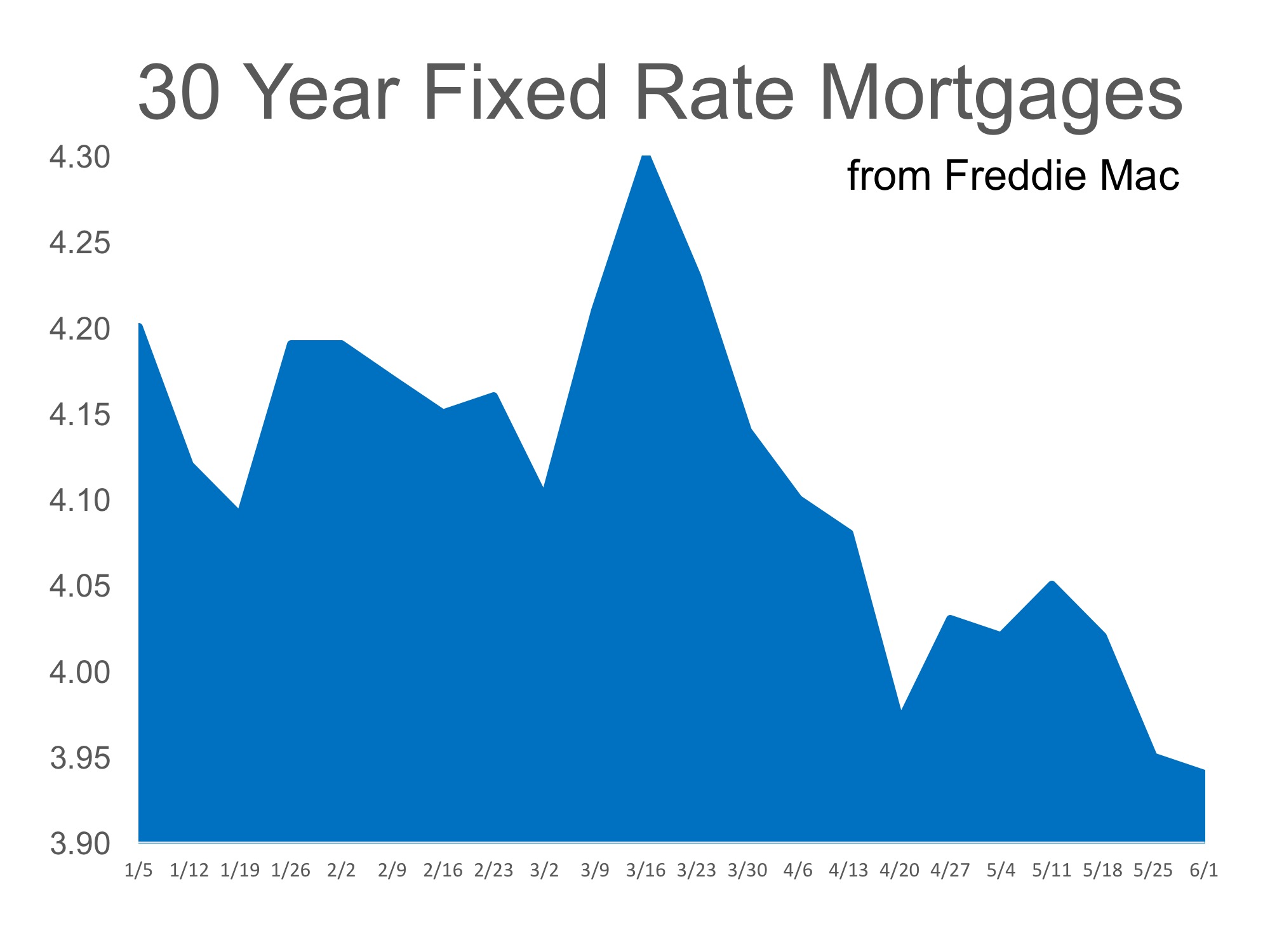

To start the year, housing experts all agreed on one thing: 2017 was going to be the year we would see mortgage interest rates begin to rise. After years of historically low rates, and an improving economy, the question wasn’t if they would increase but instead how much they would increase. Some thought we could see rates hit 5-5.5% by the end of the year.

However, the exact opposite has happened. Instead of higher rates as we head into the middle of 2017, we now have the lowest rates of the year (as reported by Freddie Mac). Here is a graph of mortgage rate movement since the beginning of the year:

Projections still call for an increase…

Four major entities (Freddie Mac, Fannie Mae, the Mortgage Bankers Association and the National